Blog

The blogs were developed with the understanding that Steiner & Wald, CPAs, LLC is not rendering legal, accounting or other professional advice or opinions on specific facts or matters and recommends you consult a professional attorney, accountant, tax professional, financial advisor or other appropriate industry professional. These blogs reflect the tax law in effect as of the date the blogs were written. Some material may be affected by changes in the laws or in the interpretation of such laws. Therefore, the services of a legal or tax advisor should be sought before implementing any ideas contained in these blogs. Feel free to contact us should you wish to discuss any of these blogs in more specific detail.

2018 Q1 tax calendar: Key deadlines for businesses and other employers

Here are some of the key tax-related deadlines affecting businesses and other employers during the first quarter of 2018. Keep in mind that this list isn’t all-inclusive, so there may be additional deadlines that apply to you. Contact us to ensure you’re meeting all applicable deadlines and to learn more about the filing requirements.

January 31

- File 2017 Forms W-2, “Wage and Tax Statement,” with the Social Security Administration and provide copies to your employees.

- Provide copies of 2017 Forms 1099-MISC, “Miscellaneous Income,” to recipients of income from your business where required.

- File 2017 Forms 1099-MISC reporting nonemployee compensation payments in Box 7 with the IRS.

- File Form 940, “Employer’s Annual Federal Unemployment (FUTA) Tax Return,” for 2017. If your undeposited tax is $500 or less, you can either pay it with your return or deposit it. If it’s more than $500, you must deposit it. However, if you deposited the tax for the year in full and on time, you have until February 12 to file the return.

- File Form 941, “Employer’s Quarterly Federal Tax Return,” to report Medicare, Social Security and income taxes withheld in the fourth quarter of 2017. If your tax liability is less than $2,500, you can pay it in full with a timely filed return. If you deposited the tax for the quarter in full and on time, you have until February 12 to file the return. (Employers that have an estimated annual employment tax liability of $1,000 or less may be eligible to file Form 944,“Employer’s Annual Federal Tax Return.”)

- File Form 945, “Annual Return of Withheld Federal Income Tax,” for 2017 to report income tax withheld on all nonpayroll items, including backup withholding and withholding on accounts such as pensions, annuities and IRAs. If your tax liability is less than $2,500, you can pay it in full with a timely filed return. If you deposited the tax for the year in full and on time, you have until February 12 to file the return.

February 28

- File 2017 Forms 1099-MISC with the IRS if 1) they’re not required to be filed earlier and 2) you’re filing paper copies. (Otherwise, the filing deadline is April 2.)

March 15

- If a calendar-year partnership or S corporation, file or extend your 2017 tax return and pay any tax due. If the return isn’t extended, this is also the last day to make 2017 contributions to pension and profit-sharing plans.

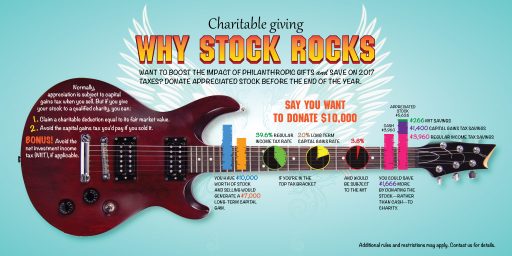

Even if your income is high, your family may be able to benefit from the 0% long-term capital gains rate

We’re entering the giving season, and if making financial gifts to your loved ones is part of your plans — or if you’d simply like to reduce your capital gains tax — consider giving appreciated stock instead of cash this year. Doing so might allow you to eliminate all federal tax liability on the appreciation, or at least significantly reduce it.

Leveraging lower rates

Investors generally are subject to a 15% tax rate on their long-term capital gains (20% if they’re in the top ordinary income tax bracket of 39.6%). But the long-term capital gains rate is 0% for gain that would be taxed at 10% or 15% based on the taxpayer’s ordinary-income rate.

In addition, taxpayers with modified adjusted gross income (MAGI) over $200,000 per year ($250,000 for joint filers and $125,000 for married filing separately) may owe the net investment income tax (NIIT). The NIIT equals 3.8% of the lesser of your net investment income or the amount by which your MAGI exceeds the applicable threshold.

If you have loved ones in the 0% bracket, you may be able to take advantage of it by transferring appreciated assets to them. The recipients can then sell the assets at no or a low federal tax cost.

The strategy in action

Faced with a long-term capital gains tax rate of 23.8% (20% for the top tax bracket, plus the 3.8% NIIT), Rick and Sara decide to transfer some appreciated stock to their adult daughter, Maia. Just out of college and making only enough from her entry-level job to leave her with $25,000 in taxable income, Maia falls into the 15% income tax bracket. Therefore, she qualifies for the 0% long-term capital gains rate.

However, the 0% rate applies only to the extent that capital gains “fill up” the gap between Maia’s taxable income and the top end of the 15% bracket. In 2017, the 15% bracket for singles tops out at $37,950.

When Maia sells the stock her parents transferred to her, her capital gains are $20,000. Of that amount $12,950 qualifies for the 0% rate and the remaining $7,050 is taxed at 15%. Maia pays only $1,057.50 of federal tax on the sale vs. the $4,760 her parents would have owed had they sold the stock themselves.

Additional considerations

Before acting, make sure the recipients won’t be subject to the “kiddie tax.” Also consider any gift and generation-skipping transfer (GST) tax consequences.

For more information on transfer taxes, the kiddie tax or capital gains planning, please contact us. We can help you find the strategies that will best achieve your goals.

You may need to add RMDs to your year-end to-do list

As the end of the year approaches, most of us have a lot of things on our to-do lists, from gift shopping to donating to our favorite charities to making New Year’s Eve plans. For taxpayers “of a certain age” with a tax-advantaged retirement account, as well as younger taxpayers who’ve inherited such an account, there may be one more thing that’s critical to check off the to-do list before year end: Take required minimum distributions (RMDs).

A huge penalty

After you reach age 70½, you generally must take annual RMDs from your:

- IRAs (except Roth IRAs), and

- Defined contribution plans, such as 401(k) plans (unless you’re still an employee and not a 5%-or-greater shareholder of the employer sponsoring the plan).

An RMD deferral is available in the initial year, but then you’ll have to take two RMDs the next year. The RMD rule can be avoided for Roth 401(k) accounts by rolling the balance into a Roth IRA.

For taxpayers who inherit a retirement plan, the RMD rules generally apply to defined-contribution plans and both traditional and Roth IRAs. (Special rules apply when the account is inherited from a spouse.)

RMDs usually must be taken by December 31. If you don’t comply, you can owe a penalty equal to 50% of the amount you should have withdrawn but didn’t.

Should you withdraw more than the RMD?

Taking only RMDs generally is advantageous because of tax-deferred compounding. But a larger distribution in a year your tax bracket is low may save tax.

Be sure, however, to consider the lost future tax-deferred growth and, if applicable, whether the distribution could: 1) cause Social Security payments to become taxable, 2) increase income-based Medicare premiums and prescription drug charges, or 3) affect other tax breaks with income-based limits.

Also keep in mind that, while retirement plan distributions aren’t subject to the additional 0.9% Medicare tax or 3.8% net investment income tax (NIIT), they are included in your modified adjusted gross income (MAGI). That means they could trigger or increase the NIIT, because the thresholds for that tax are based on MAGI.

For more information on RMDs or tax-savings strategies for your retirement plan distributions, please contact us.

Why you may want to accelerate your property tax payment into 2017

Accelerating deductible expenses, such as property tax on your home, into the current year typically is a good idea. Why? It will defer tax, which usually is beneficial. Prepaying property tax may be especially beneficial this year, because proposed tax legislation might reduce or eliminate the benefit of the property tax deduction beginning in 2018.

Proposed changes

The initial version of the House tax bill would cap the property tax deduction for individuals at $10,000. The initial version of the Senate tax bill would eliminate the property tax deduction for individuals altogether.

In addition, tax rates under both bills would go down for many taxpayers, making deductions less valuable. And because the standard deduction would increase significantly under both bills, some taxpayers might no longer benefit from itemizing deductions.

2017 year-end planning

You can prepay (by December 31) property taxes that relate to 2017 but that are due in 2018 and deduct the payment on your 2017 return. But you generally can’t prepay property tax that relates to 2018 and deduct the payment on your 2017 return.

Prepaying property tax will in most cases be beneficial if the property tax deduction is eliminated beginning in 2018. But even if the property tax deduction is retained, prepaying could still be beneficial. Here’s why:

- If your property tax bill is very large, prepaying is likely a good idea in case the property tax deduction is capped beginning in 2018.

- If you could be subject to a lower tax rate in 2018 or won’t have enough itemized deductions overall in 2018 to exceed a higher standard deduction, prepaying is also likely tax-smart because a property tax deduction next year would have less or no benefit.

However, there are a few caveats:

- If you’re subject to the AMT in 2017, you won’t get any benefit from prepaying your property tax. And if the property tax deduction is retained for 2018, the prepayment could cost you a tax-saving opportunity next year.

- If your income is high enough that the income-based itemized deduction reduction applies to you, the tax benefit of a prepayment may be reduced.

- While the initial versions of both the House and Senate bills generally lower tax rates, some taxpayers might still end up being subject to higher tax rates in 2018, either because of tax law changes or simply because their income goes up next year. If you’re among them and the property tax deduction is retained, you may save more tax by holding off on paying property tax until it’s due next year.

It’s still uncertain what the final legislation will contain and whether it will be passed and signed into law this year. We can help you make the best decision based on tax law change developments and your specific situation.

2017 might be your last chance to hire veterans and claim a tax credit

With Veterans Day on November 11, it’s an especially good time to think about the sacrifices veterans have made for us and how we can support them. One way businesses can support veterans is to hire them. The Work Opportunity tax credit (WOTC) can help businesses do just that, but it may not be available for hires made after this year.

As released by the Ways and Means Committee of the U.S. House of Representatives on November 2, the Tax Cuts and Jobs Act would eliminate the WOTC for hires after December 31, 2017. So you may want to consider hiring qualifying veterans before year end.

The WOTC up close

You can claim the WOTC for a portion of wages paid to a new hire from a qualifying target group. Among the target groups are eligible veterans who receive benefits under the Supplemental Nutrition Assistance Program (commonly known as “food stamps”), who have a service-related disability or who have been unemployed for at least four weeks. The maximum credit depends in part on which of these factors apply:

- Food stamp recipient or short-term unemployed (at least 4 weeks but less than 6 months): $2,400

- Disabled: $4,800

- Long-term unemployed (at least 6 months): $5,600

- Disabled and long-term unemployed: $9,600

The amount of the credit also depends on the wages paid to the veteran and the number of hours the veteran worked during the first year of employment.

You aren’t subject to a limit on the number of eligible veterans you can hire. For example, if you hire 10 disabled long-term-unemployed veterans, the credit can be as much as $96,000.

Other considerations

Before claiming the WOTC, you generally must obtain certification from a “designated local agency” (DLA) that the hired individual is indeed a target group member. You must submit IRS Form 8850, “Pre-Screening Notice and Certification Request for the Work Opportunity Credit,” to the DLA no later than the 28th day after the individual begins work for you.

Also be aware that veterans aren’t the only target groups from which you can hire and claim the WOTC. But in many cases hiring a veteran will provided the biggest credit. Plus, research assembled by the Institute for Veterans and Military Families at Syracuse University suggests that the skills and traits of people with a successful military employment track record make for particularly good civilian employees.

Looking ahead

It’s still uncertain whether the WOTC will be repealed. The House bill likely will be revised as lawmakers negotiate on tax reform, and it’s also possible Congress will be unable to pass tax legislation this year. Under current law, the WOTC is scheduled to be available through 2019.

But if you’re looking to hire this year, hiring veterans is worth considering for both tax and nontax reasons. Contact us for more information on the WOTC or on other year-end tax planning strategies in light of possible tax law changes.

The ins and outs of tax on “income investments”

Many investors, especially more risk-averse ones, hold much of their portfolios in “income investments” — those that pay interest or dividends, with less emphasis on growth in value. But all income investments aren’t alike when it comes to taxes. So it’s important to be aware of the different tax treatments when managing your income investments.

Varying tax treatment

The tax treatment of investment income varies partly based on whether the income is in the form of dividends or interest. Qualified dividends are taxed at your favorable long-term capital gains tax rate (currently 0%, 15% or 20%, depending on your tax bracket) rather than at your ordinary-income tax rate (which might be as high as 39.6%). Interest income generally is taxed at ordinary-income rates. So stocks that pay dividends might be more attractive tax-wise than interest-paying income investments, such as CDs and bonds.

But there are exceptions. For example, some dividends aren’t qualified and therefore are subject to ordinary-income rates, such as certain dividends from:

- Real estate investment trusts (REITs),

- Regulated investment companies (RICs),

- Money market mutual funds, and

- Certain foreign investments.

Also, the tax treatment of bond interest varies. For example:

- Interest on U.S. government bonds is taxable on federal returns but exempt on state and local returns.

- Interest on state and local government bonds is excludable on federal returns. If the bonds were issued in your home state, interest also might be excludable on your state return.

- Corporate bond interest is fully taxable for federal and state purposes.

One of many factors

Keep in mind that tax reform legislation could affect the tax considerations for income investments. For example, if your ordinary rate goes down under tax reform, there could be less of a difference between the tax rate you’d pay on qualified vs. nonqualified dividends.

While tax treatment shouldn’t drive investment decisions, it’s one factor to consider — especially when it comes to income investments. For help factoring taxes into your investment strategy, contact us.

Retirement savings opportunity for the self-employed

Did you know that if you’re self-employed you may be able to set up a retirement plan that allows you to contribute much more than you can contribute to an IRA or even an employer-sponsored 401(k)? There’s still time to set up such a plan for 2017, and it generally isn’t hard to do. So whether you’re a “full-time” independent contractor or you’re employed but earn some self-employment income on the side, consider setting up one of the following types of retirement plans this year.

Profit-sharing plan

This is a defined contribution plan that allows discretionary employer contributions and flexibility in plan design. (As a self-employed person, you’re both the employer and the employee.) You can make deductible 2017 contributions as late as the due date of your 2017 tax return, including extensions — provided your plan exists on Dec. 31, 2017.

For 2017, the maximum contribution is 25% of your net earnings from self-employment, up to a $54,000 contribution. If you include a 401(k) arrangement in the plan, you might be able to contribute a higher percentage of your income. If you include such an arrangement and are age 50 or older, you may be able to contribute as much as $60,000.

Simplified Employee Pension (SEP)

This is a defined contribution plan that provides benefits similar to those of a profit-sharing plan. But you can establish a SEP in 2018 and still make deductible 2017 contributions as late as the due date of your 2017 income tax return, including extensions. In addition, a SEP is easy to administer.

For 2017, the maximum SEP contribution is 25% of your net earnings from self-employment, up to a $54,000 contribution.

Defined benefit plan

This plan sets a future pension benefit and then actuarially calculates the contributions needed to attain that benefit. The maximum annual benefit for 2017 is generally $215,000 or 100% of average earned income for the highest three consecutive years, if less.

Because it’s actuarially driven, the contribution needed to attain the projected future annual benefit may exceed the maximum contributions allowed by other plans, depending on your age and the desired benefit. You can make deductible 2017 defined benefit plan contributions until your return due date, provided your plan exists on Dec. 31, 2017.

More to think about

Additional rules and limits apply to these plans, and other types of plans are available. Also, keep in mind that things get more complicated — and more expensive — if you have employees. Why? Generally, they must be allowed to participate in the plan, provided they meet the qualification requirements. To learn more about retirement plans for the self-employed, contact us.

2 ACA taxes that may apply to your exec comp

If you’re an executive or other key employee, you might be rewarded for your contributions to your company’s success with compensation such as restricted stock, stock options or nonqualified deferred compensation (NQDC). Tax planning for these forms of “exec comp,” however, is generally more complicated than for salaries, bonuses and traditional employee benefits.

And planning gets even more complicated if you could potentially be subject to two taxes under the Affordable Care Act (ACA): 1) the additional 0.9% Medicare tax, and 2) the net investment income tax (NIIT). These taxes apply when certain income exceeds the applicable threshold: $250,000 for married filing jointly, $125,000 for married filing separately, and $200,000 for other taxpayers.

Additional Medicare tax

The following types of exec comp could be subject to the additional 0.9% Medicare tax if your earned income exceeds the applicable threshold:

- Fair market value (FMV) of restricted stock once the stock is no longer subject to risk of forfeiture or it’s sold,

- FMV of restricted stock when it’s awarded if you make a Section 83(b) election,

- Bargain element of nonqualified stock options when exercised, and

- Nonqualified deferred compensation once the services have been performed and there’s no longer a substantial risk of forfeiture.

NIIT

The following types of gains from stock acquired through exec comp will be included in net investment income and could be subject to the 3.8% NIIT if your modified adjusted gross income (MAGI) exceeds the applicable threshold:

- Gain on the sale of restricted stock if you’ve made the Sec. 83(b) election, and

- Gain on the sale of stock from an incentive stock option exercise if you meet the holding requirements.

Keep in mind that the additional Medicare tax and the NIIT could possibly be eliminated under tax reform or ACA-related legislation. If you’re concerned about how your exec comp will be taxed, please contact us. We can help you assess the potential tax impact and implement strategies to reduce it.